FitEasy – A Hidden Compounder and Our Largest Position

Ticker: $212A.T

Have you ever seen a company growing earnings by around 60% YoY, expected to continue compounding at roughly 30% annually over the coming years, consistently beating guidance, operating in an underpenetrated market, while trading at roughly 13x EV/EBIT and still being almost completely uncovered by analysts?

We have. It is currently the largest core position in our portfolio.

And despite the stock appreciating after the latest results and guidance increase, we still see this as a very attractive opportunity – we continue to hold our full position and even added meaningfully before the latest earnings release. In this writeup we will present why.

Since this is our first post here on Substack, allow us to do a quick introduction before we dive into the company.

We are a Czech-based investment fund and research team focused on global small and mid-cap equities, compounders, and asymmetric opportunities.

Going forward, we’re planning to publish our detailed research, complete valuation models, portfolio updates, new positions, channel checks and multi-thousand-word investment theses here on our Substack. If you enjoy deep fundamental research on companies with compelling upside potential, we’d love to have you join us and subscribe for our future posts:

We increased our position before earnings

A few weeks before the latest results we decided to significantly increase our position, to ~14 % of our portfolio on the cost basis. This wasn’t because we expected a “good quarter.” It was because we believed the market was dramatically underestimating what future guidance will the management provide.

Unlike many companies, FitEasy publishes monthly membership data, giving us a real-time picture of demand. By the end of May, the company had already reached roughly 274,000 members, while management’s full-year target was 300,000 members with approximately five months still remaining in the fiscal year.

In May alone, FitEasy added roughly 15,000 new members.

Looking at those numbers, it became increasingly difficult to construct a realistic scenario in which management would not raise guidance. Even if monthly member additions slowed materially, the company would still likely exceed its original targets.

The company subsequently did exactly what we expected:

raised guidance,

doubled full-year dividend,

raised profit expectations by a lot more than revenue expectations.

In our opinion, the last point is actually the most important and it supports what has been the core of our investment thesis from the very beginning: FitEasy’s earnings should grow faster than revenue.

Why we believe the market still misunderstands the company

Most investors currently view FitEasy as simply another gym operator. We think that’s the wrong framework. In our opinion, FitEasy should increasingly be viewed as an asset-light franchise platform with multiple embedded growth engines rather than a traditional fitness chain.

Even more importantly, we believe the market is focusing on today’s reported margins instead of understanding how the revenue mix is likely to evolve over the next several years. Understanding this shift is key to seeing why this company should become a much more attractive businnes going forward.

Today, lower-margin equipment and development revenue represents a significant portion of sales because the company is opening new locations at an extraordinary pace. Many investors therefore conclude that margins are unlikely to improve significantly.

We believe exactly the opposite – as the installed franchise base grows, recurring franchise royalties should represent an increasingly larger share of revenue. Those revenues carry dramatically higher margins. That means operating profit should compound materially faster than revenue.

Notably, the latest guidance revision points exactly in this direction.

We believe management continues to guide conservatively

One observation we’ve made over the past several years is that management appears consistently conservative when setting expectations. This year wasn’t the first example.

Last year management also raised guidance during the fiscal year after originally setting fairly conservative expectations. We think the market may be relying too heavily on official guidance instead of independently modeling what the business could actually earn.

This is particularly important because FitEasy has very limited analyst coverage, so effectively, management guidance becomes market consensus. If management starts from conservative assumptions, consensus starts from conservative assumptions as well and that creates opportunities.

Why this is our largest core holding

Our investment philosophy is fairly simple.

We look for businesses where:

the underlying company compounds for many years,

valuation remains attractive,

and the market misunderstands one or more structural drivers.

FitEasy checks every box.

Today the company trades at roughly 13x EV/EBIT, despite growing substantially faster than most listed fitness companies globally. Even more importantly, we believe several structural drivers have not yet begun contributing meaningfully to earnings.

Those drivers include:

expanding franchise royalties,

increasing monetization of existing members,

AI-enabled services,

higher-margin ancillary services,

operating leverage,

and a rapidly expanding ecosystem.

The market is mostly looking at today’s gym business. We are trying to understand what this company could look like three to five years from now. And we believe this difference creates an amazing opportunity – that’s why FitEasy remains our largest position.

In the next part we’ll explain why Japan may currently be one of the most attractive fitness markets globally, why penetration still remains dramatically below Western countries, and why we believe the industry’s runway is much longer than investors currently appreciate.

PART 2 – Why Japan? One of the most overlooked fitness markets in the world

One of the biggest reasons we invested in FitEasy has very little to do with FitEasy itself. It has everything to do with Japan. When investors think about Japanese demographics, they usually think about an aging population, slow GDP growth and a shrinking workforce. Ironically, many of those same trends create an extremely attractive environment for FitEasy.

The market is still dramatically underpenetrated

One statistic immediately caught our attention. Only a few years ago, gym penetration in Japan was roughly 3% of the population. Today that figure has approximately doubled to around 6%, but it still remains dramatically below developed Western markets.

For comparison:

United States: roughly 20%

Western Europe: roughly 15–20%

Japan: approximately 6%

Even after the recent acceleration, Japan remains one of the least penetrated developed fitness markets globally. That matters because FitEasy doesn’t need to take significant market share from competitors in order to grow. The market itself is expanding rapidly. This is one of our favorite types of investments: A company operating in a market where the pie itself is getting much larger every year.

Why is Japan changing?

Historically, gyms simply weren’t part of everyday Japanese culture in the same way they are in North America. That has changed dramatically over the last several years. Several structural trends are now moving in the same direction.

1. Health awareness

Japan has one of the oldest populations in the world. Maintaining mobility, strength and overall health is becoming increasingly important. Fitness is gradually shifting from being viewed as a hobby to becoming part of preventive healthcare. That creates an enormous long-term tailwind.

2. Digitalization

Japan is rapidly adopting fully automated 24/7 gyms.

Many locations now operate with:

facial recognition,

automated access,

cashless payments,

minimal staffing.

This dramatically reduces labor costs while improving convenience. Members can visit literally any time of day. That flexibility is particularly valuable in Japan, where working hours tend to be longer and stricter than in many Western countries.

3. Labor shortages

Japan faces one of the tightest labor markets globally. Businesses that require fewer employees gain an important structural advantage.

FitEasy’s operating model is designed exactly for that environment. Automation allows the company to scale without proportionally increasing operating costs. That is another reason we expect margins to continue expanding.

4. Changing lifestyle and sports preferences

Another important trend is the shift in how younger generations approach sports. Traditionally, activities like judo, karate or baseball were far more popular than commercial gyms.

Today, people increasingly prefer flexible 24/7 fitness clubs that fit around busy schedules without requiring coaches or fixed class times. We believe this cultural shift is another structural tailwind supporting the long-term growth of fitness memberships in Japan.

FitEasy is not just an another gym

This is probably the single biggest misconception we see. Most investors compare FitEasy with traditional gyms but we think that comparison is quite off. Management is trying to build what they often describe as a lifestyle platform.

The goal is simple: Become the place people visit not only to exercise, but throughout their daily lives. Think about where people spend most of their time – at work and at home. FitEasy wants to become the “third place.” A place where members exercise… but also work, relax, recover and socialize. That distinction is incredibly important.

One membership. Many reasons to visit.

Instead of offering only workout equipment, FitEasy continues adding complementary services. Depending on the location, members may also have access to:

golf simulators

basketball courts

bouldering

beauty treatments

self-care services

oxygen capsules

recovery rooms

coworking spaces

massage equipment

wellness facilities

karaoke

arcade games

Management currently operates dozens of complementary concepts that can be integrated into different clubs. This dramatically changes the customer proposition. Members are no longer paying only for gym access – they’re buying access to an entire lifestyle ecosystem.

This creates a powerful network effect

One concern we initially had was whether opening locations close to one another would eventually cannibalize existing clubs. Interestingly, the data suggests the opposite. Because every location offers a different combination of services, additional clubs actually increase the value of the membership.

Imagine living in a city with several FitEasy locations.

Monday:

Train at the club with the wellness area.

Wednesday:

Visit the location with golf simulators.

Friday:

Go to another location with beauty services or coworking facilities.

All under the same membership.

Every new location effectively increases the number of experiences available to existing members. That is very different from a traditional gym chain. In our opinion, this network effect remains significantly underappreciated.

Social aspect & infrastructure

Another aspect that rarely receives attention is Japan’s social structure. Japan has one of the highest proportions of single-person households globally. Loneliness has become an increasingly important societal issue.

We think FitEasy benefits from becoming more than simply a place to exercise. It becomes somewhere people regularly visit, interact and spend time. Management appears to understand this extremely well.

Many of the additional services make perfect sense once viewed through that lens. They’re not random amenities. They’re designed to increase visit frequency, member engagement and ultimately customer lifetime value.

We believe the runway is still enormous

Today FitEasy operates roughly 300 locations. Yet given current penetration levels, we believe the long-term opportunity is substantially larger. Could Japan ultimately support 1,000 clubs?

Possibly.

Could it support 2,000 clubs?

We certainly wouldn’t rule it out. Management official guidance is even a bit higher. At today’s penetration, the company is still addressing only a fraction of its potential market. The important point is not predicting the exact number. The important point is recognizing that growth is unlikely to be constrained by market saturation anytime soon.

In the next section we’ll explain why we believe the market largely misunderstands FitEasy’s business model, why franchise economics are so important, and why we expect operating profit to grow materially faster than revenue over the coming years.

PART 3 – The business model the market misunderstands

If we had to summarize our entire investment thesis into one sentence, it would probably be this:

The market values FitEasy as a rapidly expanding gym operator, while we increasingly value it as a high-margin franchise platform with significant operating leverage.

That difference may sound subtle but in our opinion, it explains almost the entire valuation gap.

Looking at consolidated revenue misses the point

One of the first things we noticed when analyzing the company was that looking only at consolidated revenue gives a very misleading picture. Revenue is generated through several fundamentally different businesses.

Each has a completely different margin profile, each scales differently and each deserves a different valuation. The market, however, tends to treat them as one business. We don’t.

Instead, we built our own model estimating operating margins for each segment separately using:

FitEasy’s historical financial statements,

management commentary,

comparisons with Planet Fitness,

comparisons with Basic-Fit,

franchise economics,

and historical segment development.

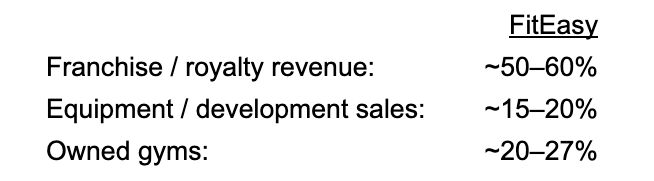

Management unfortunately does not disclose operating profitability by segment. So we attempted to estimate it ourselves. Based on our work, we estimate the approximate operating margin profile as follows:

We spent dozens of hours refining these assumptions and interestingly, the latest earnings only increased our confidence that the overall direction of the model is correct.

Current segment mix

Over the last twelve months, based on the latest quarterly data, FitEasy’s revenue mix was roughly:

Owned / directly operated gyms: ~15.5%

Recurring operational / franchise revenue: ~21.7%

Development / equipment sales: ~62.5%

That explains why consolidated margins today hide the economics of the long-term model. The largest revenue segment today is still development and equipment sales. This segment is important, but it is lower margin. It is not where the long-term earnings power sits. In our model, the mix gradually changes.

By 2028, in our base case, we model approximately:

Owned gyms: ¥2.5B revenue / ~9% of sales

Franchise revenue: ¥8.4B revenue / ~31% of sales

Development / equipment sales: ¥16.5B revenue / ~60% of sales

Total revenue: ¥27.4B (above management guidance of ¥24B)

At first glance, development revenue still remains a large share of total revenue. But the crucial difference is profit mix.

In our base case, the franchise segment generates roughly ¥4.6B of EBIT, while development sales generate roughly ¥2.5B. In other words, franchise revenue is much smaller than development revenue, but contributes far more profit per yen of sales.

That is the main point – revenue mix matters less than profit mix.

Segment 1 – Owned clubs

FitEasy owns and operates a number of corporate locations. These clubs are extremely important. Not because they generate the highest returns, but because they function as the company’s testing laboratory. New services, new layouts, new technology, new AI features, new pricing.

Everything gets tested in owned clubs first. Once management identifies what works, those concepts can gradually be rolled out across the franchise network.

In our model, we assume owned gyms can gradually improve from roughly 20% operating margin toward 22–27% over time.

The reason is simple:

higher utilization,

more members per club,

better fixed-cost absorption,

higher ARPU,

and additional monetization through services.

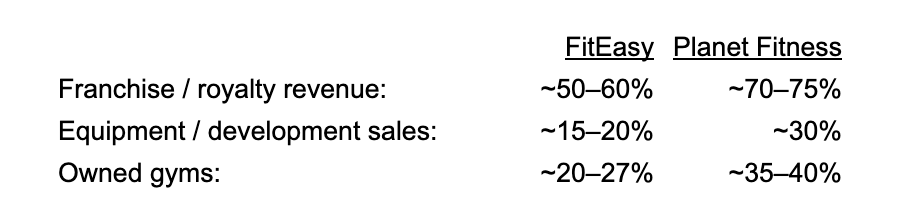

This is still well below Planet Fitness company-owned gym EBITDA margins, which are around 35–40%, so we do not view this as aggressive.

Segment 2 – Franchises

This is where our thesis becomes significantly more interesting. We believe the franchise segment ultimately becomes the primary driver of shareholder value. Why? Because franchise economics are fundamentally different. We would even argue that running a franchise network is one of the most attractive business models out there.

Instead of funding every new location with its own balance sheet, FitEasy increasingly relies on franchise partners. Those partners:

invest capital,

operate the clubs,

hire employees,

while FitEasy collects recurring fees. This dramatically improves returns on invested capital. It also means incremental revenue requires very little incremental capital.

That’s why asset-light businesses tend to deserve structurally higher valuation multiples. And the market often recognizes this only after the mix has already shifted. We think FitEasy is still early in that transition.

Based on our model, FitEasy currently generates roughly ¥10M of recurring franchise revenue per franchise location.

By 2028, depending on the scenario, we model this increasing to:

Bear: ~¥12M per franchise

Base: ~¥14M per franchise

Bull: ~¥17M per franchise

That may sound like a large increase, but we think it is reasonable given:

long-term same-store membership growth above 10%,

additional services,

higher ARPU,

AI / retail monetization,

and potential future price increases.

FitEasy’s franchise take rate also appears meaningfully higher than Planet Fitness.

Our estimate is roughly 20% for FitEasy versus around 7% for Planet Fitness.

Planet Fitness still generates more absolute revenue per gym because its clubs generate much higher sales per location, but FitEasy’s take rate is very attractive.

This is why we think the franchise segment is the most important part of the story.

Segment 3 – Equipment & development sales

Ironically, the segment that has recently grown the fastest is also the one that created the biggest misunderstanding. FitEasy sells equipment and helps franchisees build new clubs.

Naturally, this business carries much lower margins. During periods of rapid expansion, this segment becomes a larger share of revenue, mechanically depressing reported margins.

For example, in the last twelve months, development / equipment sales represented roughly 62–63% of revenue. That is why reported margins do not yet fully reflect the future economics of the company.

The market interpreted this as margin pressure. We interpreted it very differently.

To us, it simply reflects the temporary economics of building a much larger franchise network. Once those clubs open, future revenue increasingly shifts toward recurring franchise income.

The low-margin construction revenue becomes a smaller percentage of profit over time, even if it remains a large percentage of revenue. That is exactly why we believe operating margins should expand.

In our base case, we assume development revenue reaches roughly ¥16.5B in 2028 with a 15% operating margin, generating approximately ¥2.5B EBIT. In our bull case, we assume ¥18B of development revenue with a 20% operating margin, generating ¥3.6B EBIT.

The margin uplift is not based on wishful thinking. It should be achieved thanks to scale, purchasing power, standardization and the new construction license.

The construction license

Another development that we think has received surprisingly little attention is FitEasy obtaining a construction license. At first glance, this may not sound particularly exciting.

We actually think it’s strategically important. Previously, construction and fit-out work had to involve external construction companies. Now FitEasy can increasingly act as a one-stop shop for franchisees.

The company can help:

design locations,

coordinate construction,

hire subcontractors,

supply equipment,

standardize layouts,

accelerate openings.

This should improve the experience for franchisees while also allowing FitEasy to capture more economics from each new opening.

Importantly, this does not mean FitEasy becomes a capital-heavy construction company. The company can still remain asset-light by using subcontractors. But it can control more of the process and potentially capture higher margins.

That is why we believe equipment / development margins could improve from roughly 15% toward 20% over time. And more importantly, it further strengthens the ecosystem – the deeper FitEasy becomes embedded in the economics of every new club, the stronger the franchise system becomes.

Why we compare it with Planet Fitness

Throughout our research we spent considerable time studying Planet Fitness. The businesses are not identical, yet Planet Fitness provides one of the best publicly traded examples of how valuable franchise economics can become once scale is reached – as franchise royalties become a larger share of revenue, profitability can improve dramatically. FitEasy is much earlier in that journey.

Importantly, our FitEasy assumptions are materially more conservative than Planet Fitness in every segment.

(These are not perfectly comparable because Planet Fitness reports EBITDA margins while our FitEasy estimates are closer to EBIT-level operating margins. Still, we think the comparison is directionally very useful.)

Even with these conservative assumptions, FitEasy’s earnings power looks materially higher than what the market appears to be pricing today. And that is precisely why we find the opportunity attractive.

In the next part we’ll explain what we believe is FitEasy’s greatest competitive advantage: its ecosystem, exceptional same-store growth, and why member economics continue to improve despite rapid expansion.

PART 4 — FitEasy’s competitive advantage: Why we believe the market underestimates the ecosystem

If there is one metric we monitor more closely than anything else, it is monthly existing-store membership growth. Not quarterly revenue. Not reported EPS. Not even the number of new club openings.

Why? Because memberships tell us almost in real time whether our investment thesis is playing out. Financial statements are published only four times a year. Membership data is published every month. So far, the numbers continue to strengthen our conviction.

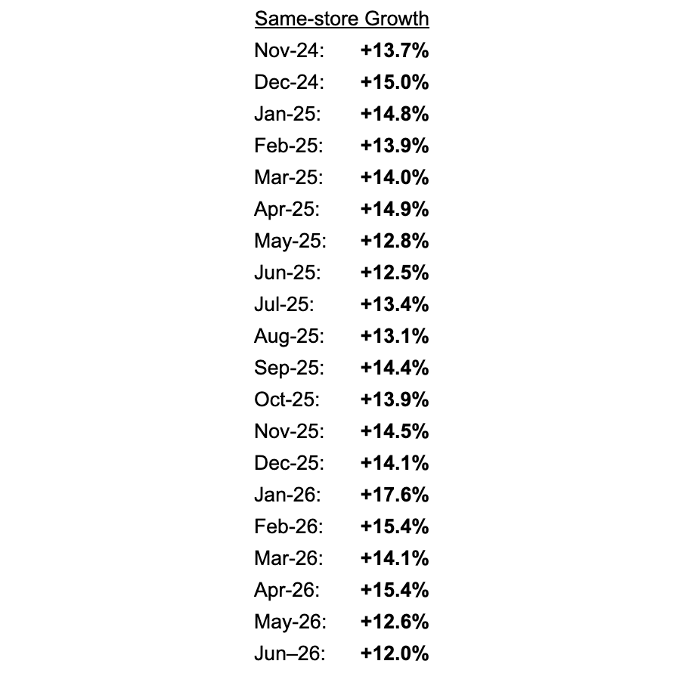

Same-store growth remains exceptional

One of the biggest concerns we had when we first started researching FitEasy was straightforward:

Would opening hundreds of new clubs eventually cannibalize existing locations?

So far, the data suggests exactly the opposite. Over the past two years, total memberships have remained remarkably consistent at around 50% YoY growth, despite the network expanding from 181 clubs in November 2024 to 281 clubs in May 2026.

Even more impressive is what happens inside mature locations. Existing-store memberships have now grown at double-digit rates for 19 consecutive months.

Recent figures include:

We have also attached the company’s yearly membership chart below because it shows the long-term member retention and because we believe it is one of the strongest pieces of evidence supporting our thesis.

For comparison, many mature Western gym operators would be pleased with 2–3% same-store sales growth. FitEasy continues delivering membership growth several times higher while simultaneously opening dozens of new clubs every year.

To us, this is one of the clearest indications that the business is still far from saturation.

We believe revenue per club can grow even faster

Interestingly, member growth may not even tell the whole story. Our expectation is that same-store revenue growth could exceed membership growth.

Why? Because management is continuously increasing the monetization opportunities available inside each location. Every additional service increases the value of the membership. Every additional service creates another opportunity to generate revenue without building another gym, leading to significant operating leverage.

The company is gradually transforming a simple gym membership into a broader lifestyle subscription. As we mentioned previously, members can already access more than 30 complementary services beyond traditional fitness equipment like golf simulators, bouldering or basketball courts and no single location offers all of them.

On top of that, the company is investing in several new monetization initiatives, including:

AI-powered personal training,

movement analysis,

personalized workout plans,

nutrition recommendations,

automated retail,

protein and supplement sales,

premium wellness services,

and, over time, higher average membership pricing.

As a result, we believe same-store revenue growth could exceed same-store membership growth, as revenue per member continues to increase.

Management continues to overdeliver

Another reason we remain confident is management’s execution. Since becoming a public company, management has consistently delivered above its original expectations.

Over the past several years they have:

repeatedly exceeded membership targets,

raised guidance during the fiscal year,

increased profit guidance by more than revenue guidance,

doubled the annual dividend,

expanded the ecosystem,

introduced new AI initiatives,

and recently obtained a construction license that should further improve the franchise offering.

Combined with one of the strongest same-store membership growth profiles we have found globally, we believe this creates a business that deserves a structurally higher valuation multiple than the market currently assigns.

In the final part, we’ll present our valuation model, expected margin expansion, scenario analysis, and why we believe FitEasy offers one of the most attractive long-term risk/reward opportunities in global small-cap equities.

PART 5 – Valuation, scenarios and why we believe FitEasy is still significantly undervalued

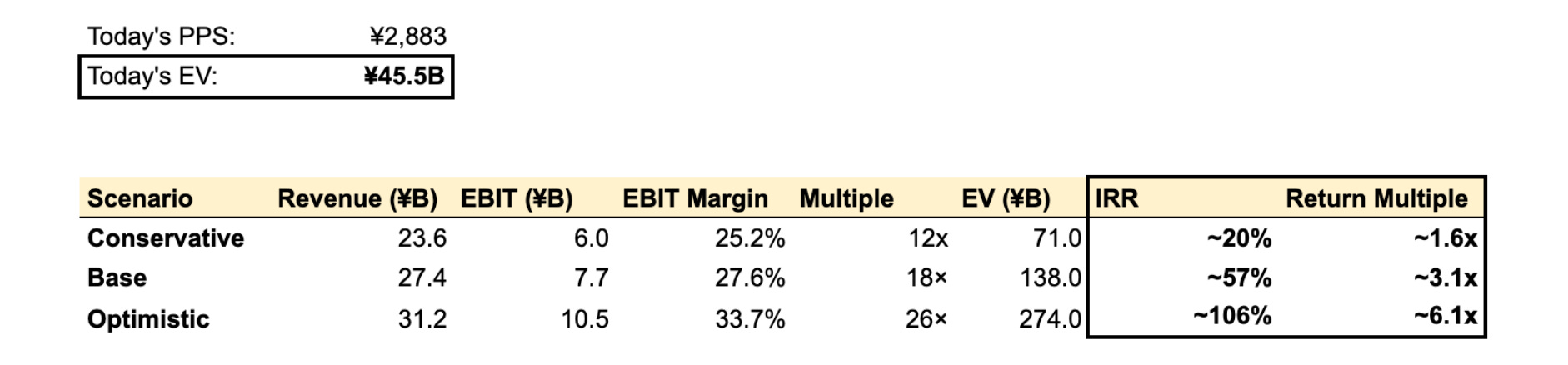

Everything ultimately comes down to one question: How much could FitEasy be worth by FY2028 if the business develops the way we expect?

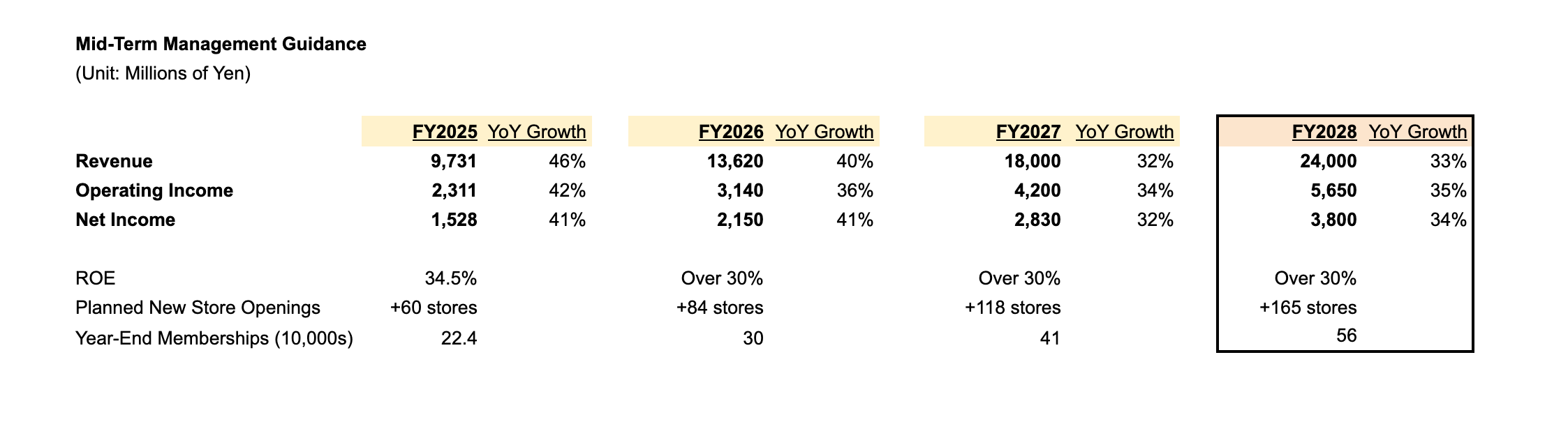

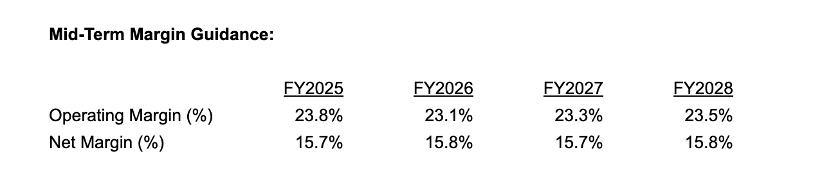

Management’s current mid-term guidance is already impressive:

We believe this guidance is still conservative, especially on profitability. The key difference between management guidance and our model is not only revenue growth – it is segment mix and margin expansion. As you can see in the margin guidance below, management actually doesn’t project any margin expansion at all:

After studying the business and management guidance in depth, we have modeled these three future scenarios:

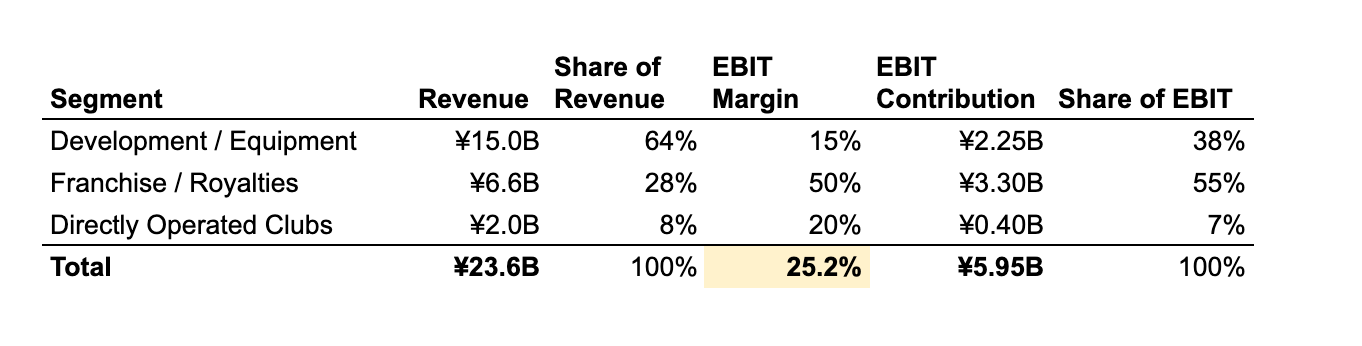

1. Conservative scenario

In our conservative case, FitEasy opens 150 new clubs in FY2028.

Revenue reaches ¥23.6B, broadly in line with management guidance.

Segment revenue mix:

Compared with management’s FY2028 guidance:

Revenue: ~2% below guidance

EBIT: ~5% above guidance

At 12x EBIT, this implies an enterprise value of roughly ¥71B. Compared with today’s EV of approximately ¥45B, that implies:

~1.6x return

+58% upside

roughly 20% annualized return over ~2.5 years.

This is the scenario where almost everything goes only reasonably well.

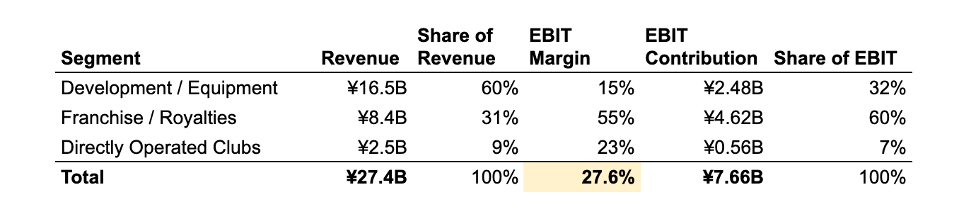

2. Base case

This is currently our most realistic scenario.

We assume FitEasy opens 165 new clubs in FY2028, broadly in line with management’s own store opening plan.

Revenue reaches ¥27.4B, meaningfully above guidance.

Segment revenue mix:

Compared with management’s FY2028 guidance:

Revenue: ~14% above guidance

EBIT: ~36% above guidance

This is the core of our thesis.

Even though franchise revenue would represent only about 31% of total revenue, it would contribute roughly 60% of total EBIT.That is why we believe earnings can grow faster than revenue.

At 18x EBIT, this implies an enterprise value of roughly ¥138B. Compared with today’s EV of approximately ¥45B, that implies:

~3.1x return

+207% upside

roughly 57% annualized return over ~2.5 years.

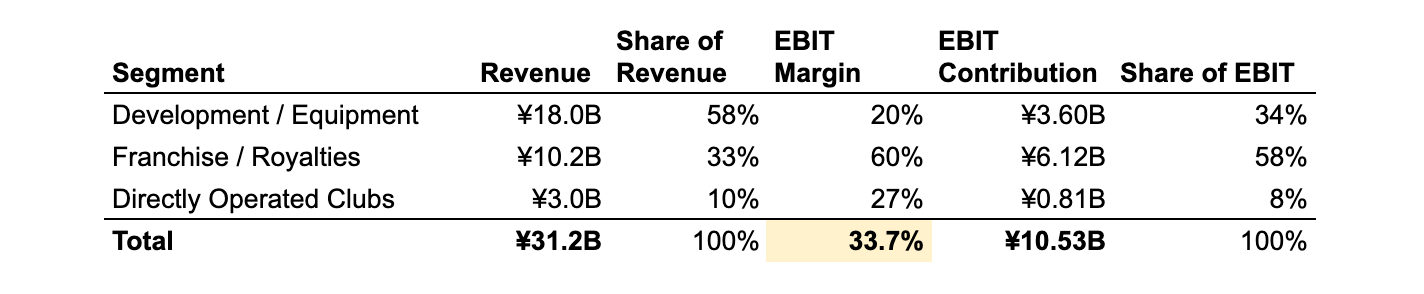

3. Optimistic scenario

This is our upside case, not our central expectation. Here we assume FitEasy continues outperforming, same-store growth remains very strong, monetization improves materially, and the market begins valuing the company more like a premium global compounder.

We assume 180 new clubs in FY2028.

Revenue reaches ¥31.2B.

Segment revenue mix:

Compared with management’s FY2028 guidance:

Revenue: ~30% above guidance

EBIT: ~86% above guidance

At 26x EBIT, this implies an enterprise value of roughly ¥274B. Compared with today’s EV of approximately ¥45B, that implies:

~6.1x return

+509% upside

More than 100% annualized return over ~2.5 years.

We view this as an optimistic scenario, but not impossible if current trends continue.

Summary of the scenarios & outcomes

The market seems to focus mainly on consolidated revenue and management guidance. We think the more important question is: What percentage of future EBIT comes from high-margin franchise royalties?

In our base case, franchise revenue is only 31% of sales, but around 60% of EBIT. That is the operating leverage the market is missing and why we believe FitEasy can outperform management guidance, especially on profitability.

Summary of the outcomes and potential returns:

Conclusion – Why FitEasy remains our largest position?

At a first sight, FitEasy looks like an average gym chain trading at a low valuation. But as we dive deeper, we find something completely different – a well-managed company operating in a growing and largely unpenetrated market.

Given expanding offerings and improved monetization, we believe FitEasy is on track to sustain its 10%+ same-store growth, and combined with new locations, this should allow them to safely beat their 30%+ revenue growth guidance in coming years. And as the company shifts more towards high-margin franchise revenue, this should also lead to structurally better margins.

Combine this with the company becoming bigger, receiving analyst coverage and institutional/index buying, and we have a recipe for a very attractive setup – potentially over 3x return in the base case. And that’s why we believe FitEasy offers one of the most attractive long-term risk/reward opportunities in global small-cap equities today.

Disclaimer: This post is for informational purposes only and is not investment advice. It reflects the author's personal views and estimates, which may be incomplete or incorrect. Do your own research and consult a qualified advisor before making investment decisions. The author/affiliated fund currently holds a position in $212A.T and may buy or sell shares at any time.

Would be curious what SSS are for competitors? Is them taking share or is the industry just doing so well given rapidly changing trends starting from a very low base

Great writeup! Do you think low cost gyms pose any threat? I know Fit Easy's positioning is more 3rd place but the high growth low cost operators have consistently taken market share from mid-end or premium tiers in Europe and US (i.e. Bfit and Planet)